If you are a real estate agent, broker or realtor in Canada and thinking to incorporating your real estate practice this blog will cover the basics that you must need to know. This blog will guide you through the process, benefits, requirements, and differences between a PREC and a standard corporation. Additionally, we will introduce how RegiCorp can assist you in this journey as an official intermediary.

What is a Personal Real Estate Corporation (PREC)?

A Personal Real Estate Corporation, also know as “PREC” is a legal entity that allows real estate agents in Canada to operate their businesses through a corporation.

This corporate structure offers licensed real estate professionals (real estate agent, brokers and realtors) various financial and operational benefits. PREC is actually designed a unique need for real estate practitioners and providing them with opportunities for tax planning, income splitting, and asset protection.

Personal real estate corporations mainly provide real estate or real estate related ancillary services. Only licensed real estate agent, broker or realtor can incorporate Personal real estate corporation. And the licensed real estate salesperson must be the sole voting shareholder also known “controlling shareholder”, owing all equity shares with voting rights. Only the controlling shareholder be director/officer of their personal real estate corporation.

In Ontario, on October 1st, 2020, was enacted new legislation for real estate agents and brokers to incorporate personal corporation. But other jurisdictions that have similar legislation, including Alberta, British Columbia, Saskatchewan, Manitoba, Quebec, and Nova Scotia.

Is a PREC professional corporation?

According to the Business Corporations Act, a PREC is not a professional corporation. And Income Tax Act also not considers a Personal Real Estate Corporation (PREC) as a professional corporation.

The term “professional corporation” defines a corporation that is carry on the professional practices of certain professionals such as accountants, dentists, lawyers, medical doctors, veterinarians, and chiropractors and so on.

While a PREC allows a real estate professional to incorporate a personal corporation but it does not fall under the specific definition of a professional corporation as per Business Corporations Act. Therefore, it also does not carry the same obligations and regulations that apply to professional corporations in the aforementioned fields.

Although, a PREC enables real estate agents, brokers, and realtors to incorporate and manage their business operations through a corporate legal entity, it is not categorized & considered as a professional corporation within the meaning of the Income Tax Act.

Requirements for Incorporating an Ontario Personal Real Estate Corporation

To incorporate a PREC in Canada, the following requirements must be met:

- Real Estate License: PREC’s controlling shareholder must be a licensed/ registered real estate professional in Canada or the specific jurisdiction.

- Equity and Share: Only the controlling shareholder have all voting right and owning all equity. Family members can be non-voting shareholders.

- Articles of Incorporation: The corporation must file Articles of Incorporation with the appropriate provincial authorities.

- Regulatory Compliance: PREC regulations are set by designated body. A PREC must comply with that regulations set by the Real Estate Council or any other relevant regulatory bodies like Real Estate Council of Ontario (RECO) in Ontario.

- Only Director: Controlling shareholder be the only one director of PREC.

- Be the president: Controlling shareholder be the only president of PREC.

Can a Group of Real Estate Agents form a Personal Real Estate Corporation (PREC)

A PREC must be a single person corporation. So, a group of real estate agents cannot collectively form a single Personal Real Estate Corporation (PREC). According to PREC regulations a PREC must be controlled by a single, licensed real estate professional. Every real estate agent, realtor and broker must form their own individual PREC like a single person-controlled corporation.

Example Scenario:

Suppose three real estate agents, Jane, John, and Lisa, want to incorporate and take advantage of the benefits of a PREC, each must form their own PREC:

- Jane Doe Professional Real Estate Corporation

- John Smith Professional Real Estate Corporation

- Lisa Brown Professional Real Estate Corporation

They can work together as a team and even can share resources, but every agent’s PREC must mange and control independently.

Advantages of incorporating a Personal Real Estate Corporation (PREC)

A Personal Real Estate Corporation (PREC) has several significant advantages for licensed real estate professionals. A PREC have the opportunities for tax savings, tax deferral, and income splitting. Here’s some explanation of these benefits:

Tax saving: Lower Corporate Tax Rate

In Ontario, federal and Ontario corporate tax rate combinedly is 12.5 per cent (13.5% in BC.) on the first $500,000 of business income. And general corporate rate of 26.5 per cent when income above $500,000. On the other hand, in Ontario the highest personal tax rate is 53.53 per cent on income over $220,000.

Because Individuals are taxed higher than corporate tax. When a Real estate agent incorporates a PREC he can take this tax advantages. Thus way, a PREC benefits from the small business tax rate, which is significantly lower than the personal income tax rate.

For an Example: Abraham’s PREC earns $200,000 in a year. He will pay only pays 12.2% corporate tax on this income, instead of paying up to 53.53% in personal income tax. He can save tax 41.33 per cent (53.53-12.2= 41.33%).

Tax Deferral:

One of the most significant benefits of forming a PREC is tax deferral.

A PREC can retain earnings within the corporation rather than distributing all profits to the owner in the form of salary or dividends. This retained income is taxed at the lower corporate tax rate.

From Ontario’s Real Estate Association (OREA) “By forming a PREC you are able to leave a portion of your business income in your PREC, deferring the personal taxes on this income until you decide when the PREC pays this to you as either a salary or dividend. Having more available to invest in the PREC allows you to earn more investment income and this builds your retirement portfolio more rapidly.

Deferring a portion of your current income also allows you to “smooth” the recognition of your career earnings over your lifetime. Shifting the recognition of personal taxable income from your peak earning years to your retirement years means that when you do eventually have the income paid to you by the PREC you’ll be subject to a lower marginal tax rate. For example, if you are earning over $220,000 today and project that your retirement income will be $90,000 then the tax rate on a shifted dividend from the PREC drops from 47.74 per cent to 25.16 per cent.”

By deferring the distribution of income, real estate professionals can control when they receive the income, potentially timing it to align with lower personal tax rates in future years.

Example: A real estate agent’s PREC earns $200,000 in a year. The agent decides to take only $100,000 as salary or dividends and retains the remaining $100,000 within the corporation. The retained earnings are taxed at the corporate rate, deferring the personal tax liability on that income until it is withdrawn in future years.

Income Splitting: with Family Members

In a PREC, real estate agent is the only one voting shareholder with owning all equity. But family members (spouse or children) are allowed to own non-voting shares in a PREC. Spreading the income among individuals can reduce the overall family tax burden.

However, Income splitting isn’t available to all real estate agents under the PRECs accordingly updated Tax on Split income (TOSI) rules which requires dividends paid to family members to be taxed at the highest marginal tax rate. However, there are many exceptions to TOSI. The exceptions to TOSI rules are:

- if a family member over the age of 18 works for 20+ hours per week in the PREC, they may be paid dividends that will be taxed regularly at their respective dividend tax rate (instead of TOSI’s highest marginal tax rate)

- If a real estate agent is over the age of 65

- Family members will be considered as active member, if they have worked at least an average of 20 hours per week for five years. These five years do not need to be consecutive.

If you or your family member meet these exemptions, income splitting could be a major advantage of a PREC.

Example: Jane issues non-voting shares to her spouse and pays them $20,000 in dividends. Her spouse is in a lower tax bracket, which reduces the family’s overall tax burden. Additionally, Jane’s son assists with marketing and receives a $10,000 salary, further distributing the income within the family.

Limitations of a Personal Real Estate Corporation

While a PREC offers various benefits to real estate professionals, it also comes with limitations that must be carefully considered before incorporating a PREC. Carefully, understanding these limitations helps you in making decision about whether incorporating a PREC is the right choice for you.

Limited Business Activities:

Under section 10.6(1)(e) of the Regulation, a personal real estate corporation may not “conduct any business other than the provision of real estate services and ancillary services directly associated with the provision of real estate services”.

A personal real estate corporation may not trade in stocks or bonds, other than modest trading in stocks and bonds that constitute a capital gain. Also, Restrictions can vary by province. For example, Ontario does not have any restrictions on real estate holdings, and beyond restrictions on trading of real estate.

PREC Licensing fees:

There is fee for PREC licencing. Realtors are required to apply for a PREC license as well as maintain own real estate services license. For example, if you are in Alberta, it would cost you $1,300 a year. And if it is in British Columbia, your licensing fees will total to $2,900 every two years.

Naming Requirements:

Naming requirements vary from province by province. For example, Ontario has no naming requirements. Name of a Personal Real Estate Corporation must be registered as either relator’s Legal Name or Licensee Name and must be followed by “Personal Real Estate Corporation”,

Advertising Restrictions:

Personal real estate corporations must comply with BCFSA’s advertising requirements for advertising.

If you advertise a personal real estate corporation, you must only use the licensee’s name of the personal real estate corporation in your advertising. This includes advertisements in websites, social media, other print advertising, television and radio.

It is not you, as an individual, who are providing the services on behalf of your brokerage, but rather your personal real estate corporation.

When licensing a personal real estate corporation, make sure that the legal name of the personal real estate corporation is the name in which you wish to advertise. Using the term PREC is not permitted. You must use the entire “personal real estate corporation” term.

Incorporation & Maintenance Costs:

To incorporate a PREC are typically cost around $1200-$2500 for Lawyer and legal fees. But no worries RegiCorp give you guarantee the lowest cost for incorporating you PREC. There is also some ongoing cost like bylaw & minutes book, Annual Return, bookkeeping and so on.

How to Register for a Personal Real Estate Corporation in Ontario

As of October 1, 2020, real estate agents, Realtors and Brokers in Ontario are allowed to form Personal Real Estate Corporations.

To register for a PREC in Ontario, real estate agents must get approved and give notice to the Real Estate Council of Ontario (RECO). In Ontario, it is required to have PREC head office address in Ontario. You must file your Articles of Incorporation for your PREC. To File articles of incorporation click below link:

How to Register for a Personal Real Estate Corporation in Alberta

The Real Estate Council of Alberta (RECA) is the governing body for Alberta’s real estate brokerage. The Real Estate Council of Alberta regulates real estate licensees in Alberta.

To register a PREC in Alberta you need a Alberta NUANS Report to check your PREC name’s availability. You also need to file articles of incorporation, a valid Alberta ID and Notice of Directors (you be the only director of your PREC).

If you are out of province real estate agent you must need a licence to trade in Alberta.

How to Register for a Personal Real Estate Corporation in BC

To incorporate a PREC in BC, you must apply or a license for your Personal Real Estate Corporation with the Real Estate Council of British Columbia (RECBC).

You also need a BC name reservation report to approve your PREC’s propose name. You may need to Register for a GST number and workplace insurance with WorkSafeBC.

In BC, Real estate licenses are valid for two years. When registering a Personal Real Estate Corporation for the first time, a one-time fee will be charged

How to Register for a Personal Real Estate Corporation in Saskatchewan

In Saskatchewan, naming of a PREC is different from the other provinces and include [Real Estate Agent’s Full Name], followed by “Real Estate Professional Corporation”, “Real Estate Prof. Corp.”, or “Real Estate P.C.”.

Before registering a PREC in SK you must need to ensure that your proposed PREC name is available to use as corporation name. After registering you must apply to the Saskatchewan Real Estate Commission for a Permit for your PREC. After approval, you will be issued an annual permit valid from January 1 to December 31.

How to Register for a Personal Real Estate Corporation in Nova Scotia

To incorporate for an Approved Sales Corporation License in Nova Scotia you have to follow the following steps:

- Select an appropriate name for your “Approve Sales Corporation”. The Nova Scotia Real Estate Commission requires the name of your “Approved Sales Corporation to be your first name and your last name followed by the word “Licensed”.

- Send your business name to the Licensing Officer of the Nova Scotia Real Estate Commission to approve with the subject line “Approved Sales Corporation Name”.

- Check that the selected name of your business is available for use.

- File an application for incorporation with RegiCorp (optional)

- Apply for the “Approved Sales Corporation License” with all corporation’s Registration documents, and licensing fee.

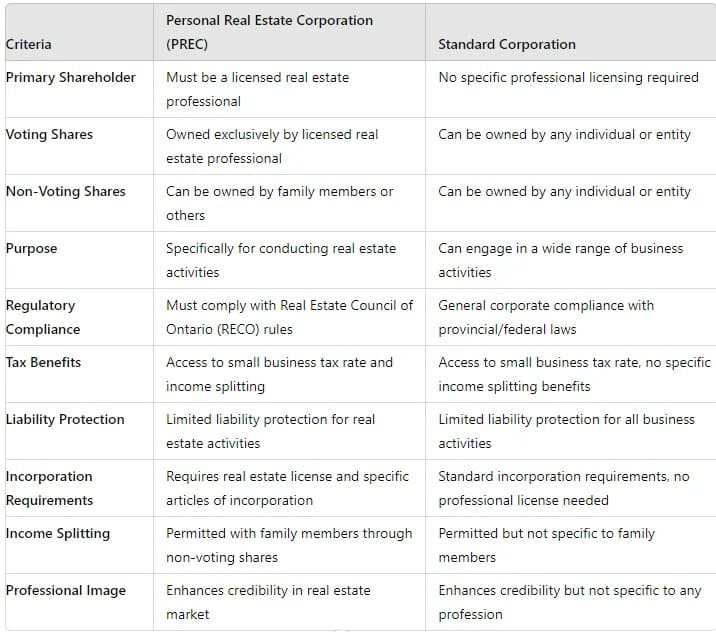

Differences between Personal Real Estate Corporation (PREC) and standard corporation:

Here’s a comparison to differentiate between a PREC and a Standard Corporation

Frequently Asked Questions (Faq's)

Can a PREC be used for passive investment purposes?

Yes, a PREC can engage in activities such as passive investing, although there may be tax and other implications. It is important to consult with a lawyer or accountant for specific advice.

What are the obligations of a registrant concerning RECO registration when using a PREC?

The PREC itself does not need to be registered with RECO. However, the controlling shareholder must be a registrant and must notify RECO when using a PREC.

Are RECO or TRESA regulations required in a PREC’s Articles of Incorporation in Ontario?

No, TRESA regulations do not mandate specific criteria for inclusion in a PREC’s Articles of Incorporation. Including such provisions may provide clarity and prevent changes that could disqualify your PREC.

Do I need to transfer the license of my PREC if I move to a different brokerage?

No, the PREC does not require a license. However, you will need a new agreement with the new brokerage and must notify RECO appropriately.

If I am part of a team with a PREC, will I receive payments from the PREC?

No, each REALTOR® must form their own PREC. Regulations do not allow multiple REALTORS® to use a single PREC. Each PREC must be individually controlled by one REALTOR®.

Can a non-equity shareholder in a PREC engage in real estate activities, such as flipping and selling homes?

A non-equity shareholder who is not a registrant does not gain additional rights to engage in real estate activities. They can only engage in activities exempt under section 5 of the Act.

Is my PREC considered a professional corporation under the Income Tax Act if it allows me to carry out my profession?

No, the term “professional corporation” in the Income Tax Act is specific to certain professions like accountants, dentists, lawyers, medical doctors, veterinarians, and chiropractors, and does not apply to PRECs.

What you need to Know!

This article is intended for general informational purposes only and should not be construed as offering legal, financial, or other professional advice. While the information presented is believed to be accurate and current, Regicorp Inc. does not guarantee its exactitude, and it should not be considered an exhaustive analysis of the covered topics. All expressed opinions reflect the authors’ judgments as of the publication date and are subject to change. Neither Regicorp Inc. nor its affiliates expressly or implicitly endorse any third parties or their recommendations, opinions, information, products, or services.For specific situations, please consult a professional advisor.